In a turbulent market session, the Nasdaq Composite entered correction territory, partly driven by Meta’s underwhelming forecast, and Alphabet’s disappointing results added to the pressure. The S&P 500 briefly touched correction territory, and Wall Street grappled with concerns about the US economy’s outlook. Meanwhile, the US dollar displayed resilience on the back of strong Q3 GDP growth. In the currency market, the dollar saw fluctuations as the Federal Reserve and European Central Bank were expected to make rate decisions. The Japanese yen faced the risk of intervention from the Ministry of Finance. The British pound and Australian dollar saw rebounds. Upcoming economic data releases are poised to continue influencing market dynamics.

Stock Market Updates

The Nasdaq Composite extended its decline into correction territory as Meta, the parent company of Facebook, reported a forecast that fell short of investors’ expectations. The tech-heavy index dropped by 1.76% on Thursday, closing at 12,595.61, falling below its 200-day moving average. The S&P 500 also dipped 1.18% to close at 4,137.23, with the Dow Jones Industrial Average slipping 0.76%, shedding 251.63 points to end at 32,784.30. The S&P 500 briefly entered correction territory during the session, marking a nearly 10% decline from its peak in July. The Nasdaq Composite officially entered correction territory, down more than 10% from its yearly high. Wall Street seemed unimpressed with recent big-tech earnings reports, with concerns about the weakening outlook for the US economy. Meta reported a beat on both top and bottom lines in the third quarter but noted advertising softness and concerns about cost control, leading to a 3.7% drop in Meta’s shares.

This decline in the stock market was influenced by a challenging trading session on Wednesday, driven by a 9.5% decline in Google-parent Alphabet, which had its Class-A shares experience their worst day since March 2020 after disappointing results in the Google cloud unit. The market’s recent correction since the summer has been partly attributed to rising bond yields, with the 10-year Treasury yield crossing 5% earlier in the month. Despite a slight decrease in the 10-year yield to 4.84% on Thursday, it did not halt the market sell-off. The market also didn’t receive a boost from the stronger-than-expected third-quarter gross domestic product (GDP) report, with the US GDP growing at a 4.9% annualized rate from July through September, surpassing the 4.7% forecast by economists. Furthermore, major earnings reports are on the horizon, with Amazon scheduled to release its results after the market’s close.

Data by Bloomberg

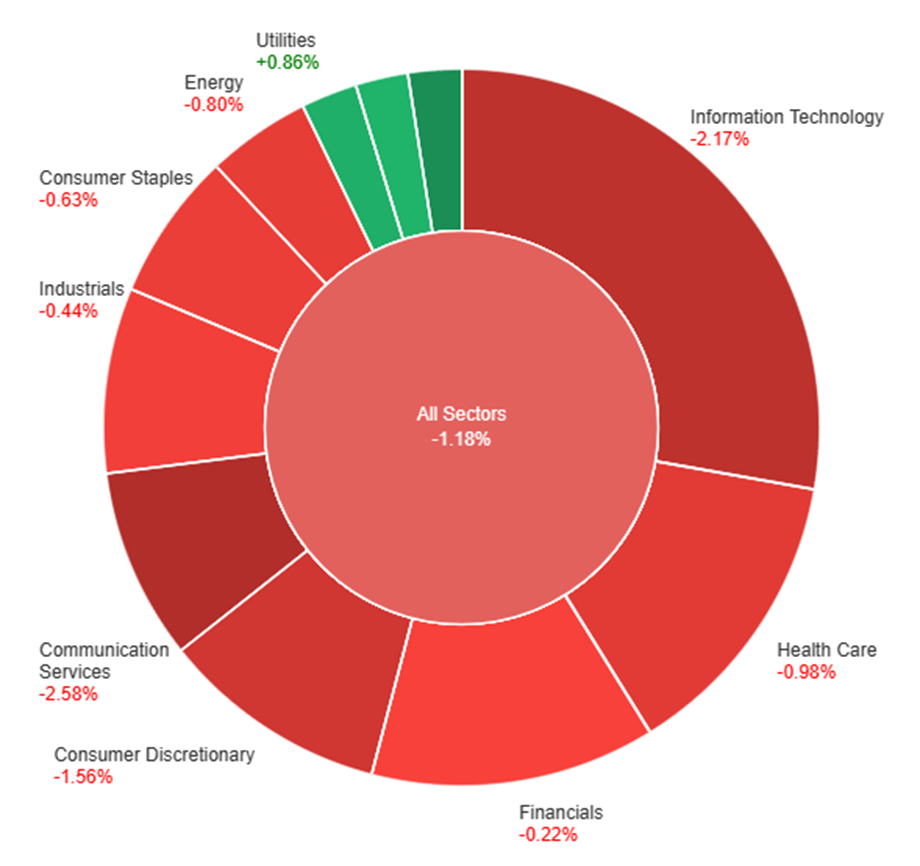

On Thursday, various sectors experienced fluctuating performance in the market. Real Estate and Utilities showed positive gains, with increases of 2.15% and 0.86%, respectively. However, Information Technology and Communication Services had a rough day, with notable declines of 2.17% and 2.58%. Overall, the broader market, represented by “All Sectors,” saw a decrease of 1.18%, while several sectors, including Consumer Discretionary, Health Care, and Consumer Staples, also ended in the red with declines ranging from 0.63% to 1.56%.

Currency Market Updates

In the latest currency market updates, the US dollar displayed resilience as it strengthened by 0.1%, despite a minor retreat in Treasury yields. This rally was prompted by robust US economic data, as Q3 GDP grew impressively at a 4.9% rate. However, the sales and core PCE figures fell short of expectations, with core PCE at 2.4% compared to 3.7% in the previous quarter. While September core capital goods orders exceeded forecasts, initial and continued jobless claims saw an increase, signaling potential challenges in finding new employment. Additionally, pending home sales surpassed expectations but remained notably weak. The EUR/USD pair experienced a 0.05% decline, with the dollar gaining momentum as both the Federal Reserve and the European Central Bank (ECB) were expected to cease their rate hikes and potentially cut rates by mid-year. The USD/JPY pair rose by 0.1%, although it had retreated from its 2023 highs at 150.78 due to a decline in Treasury yields and market concerns about the Bank of Japan’s future policy decisions. Despite these fluctuations, the main perceived risk in the currency market is the possibility of the Ministry of Finance (MoF) resuming yen buying to prevent a breakout above 2022’s 32-year high at 151.94.

Meanwhile, the British pound saw a 0.2% increase in value after hitting its lowest level since October’s 1.2038 trend lows. This rebound came in the wake of a pullback in Treasury yields, despite concerning reports of CBI sales and reduced UK public inflation expectations. The Australian dollar also displayed resilience with a 0.3% increase, recovering from its lows in 2023. This recovery was attributed to a potential change in the Reserve Bank of Australia’s policy outlook.

Looking ahead, upcoming economic data releases include Tokyo core CPI for October, expected to remain steady at 2.5%, as well as German GDP and retail sales figures. Additionally, the US market will be closely monitoring data on personal income, spending, core PCE, and Michigan sentiment. These indicators will likely continue to influence the dynamics of the currency market in the days to come.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Finds Support Despite Dovish ECB Stance and Robust US Growth Data

The EUR/USD pair hit a bottom at 1.0521, aligning with the previous week’s lows. This drop came as the European Central Bank (ECB) adopted a more dovish stance, hinting at a possible terminal interest rate amidst economic concerns. Meanwhile, the US Dollar failed to capitalize on better-than-expected US GDP figures, as the Core PCE remained slightly below expectations and employment data raised concerns. Despite these dynamics, the fundamental factors suggest a mixed outlook for EUR/USD, with potential influences from upcoming US Core PCE data.

According to technical analysis, the EUR/USD consolidated on Thursday, approaching the middle band of the Bollinger Bands. Currently, the EUR/USD is trading between the middle and lower bands, indicating the potential for further downward movement. The Relative Strength Index (RSI) is at 43, signaling that the EUR/USD is adopting a bearish bias.

Resistance: 1.0616, 1.0705

Support: 1.0500, 1.0405

XAU/USD (4 Hours)

XAU/USD Resilient as Economic Uncertainties Persist Amid ECB and US GDP Reports

Spot Gold initially surged to $1,993.44 an ounce before receding, influenced by key developments in global economics. The European Central Bank opted to keep rates unchanged due to the Euro Zone’s economic struggles, while the US Dollar strengthened following a robust Q3 GDP report. The uncertain economic outlook drove investors to seek safety in Gold, contributing to its rebound as stock markets faced headwinds.

According to technical analysis, XAU/USD is consolidating on Thursday and has the potential to reach the upper band of the Bollinger Bands, which is currently squeezing. Presently, the price of gold is consolidating near the upper band, implying a possible downward consolidation. The Relative Strength Index (RSI) is currently at 57, indicating a neutral bias for the XAU/USD pair.

Resistance: $1,985, $2,002

Support: $1,970, $1,959

Economic Data

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| USD | Core PCE Price Index m/m | 20:30 | 0.3% |

| USD | Revised UoM Consumer Sentiment | 22:00 | 63.0 |